Blockchain Explained: A Technology of Unlimited Applications

One game-changing innovation is turning traditional industries on their heads and reinventing the way we transact. Intrigued? Keep reading to discover how blockchain is transforming the landscape of finance and beyond.

Get ready for a crash course in "blockchain" — that unbreakable digital ledger that's shaking up everything from finance to healthcare.

Picture a world where trust, transparency, and innovation converge, transforming industries and redefining the way we interact. Blockchain, the groundbreaking technology that has captured the imagination of visionaries across the globe, promises to be that catalyst of change. However, regardless of being the talk of the town for a while, for many, blockchain remains shrouded in mystery. But fear not, because beneath all the complicated tech lies a concept so brilliantly simple, you'll wonder why it took you this long to "get it."

As blockchain is here to stay, it’s best to “get it” sooner rather than later, so join us on this informative quest as we dive into the seemingly infinite applications of this amazing technology.

What Is Blockchain?

Blockchain is a revolutionary technology that enables secure and transparent data sharing. Unlike traditional databases where information is stored centrally, blockchain networks distribute and synchronize data across nodes. These nodes, which can represent individuals, organizations or entire networks, use cryptography to validate updates to the blockchain. By incentivizing nodes with digital rewards, blockchain eliminates the need for a central authority.

Blockchain allows for an immutable record of transactions and data exchanges. Once information is recorded on the blockchain, it cannot be modified or removed, enabling the transfer of anything of value, physical or digital.

Here are the three key attributes of blockchain:

- First, blockchain networks are cryptographically secure, requiring both a public address and a private key for access.

- Second, blockchain operates digitally, with all transactions and records occurring online.

- Finally, blockchain networks are distributed, with data shared across all nodes in a public, private or hybrid network.

Public blockchains like Bitcoin are open for anyone to participate in. Private blockchains are more applicable to regulated industries, restricting access to approved participants with verified identities. Hybrid and consortium blockchains incorporate aspects of both public and private networks.

How Blockchain Works

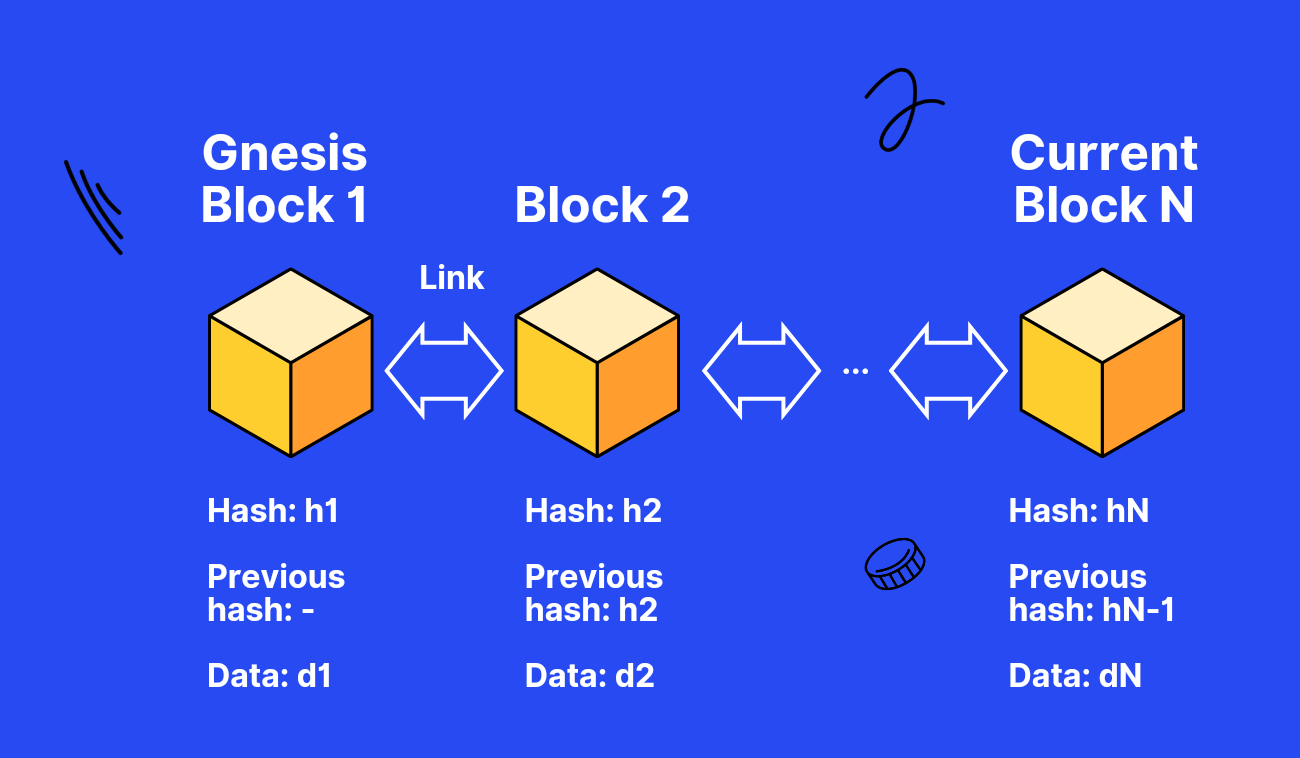

Blockchain records data in encrypted "blocks" that are chained together chronologically (Pic. 1). Each block contains a timestamp and a link to the previous block in the chain. New blocks are appended to the chain in a linear, immutable sequence.

Once recorded, blockchain data cannot be altered or removed. Transactions are encrypted with algorithms like SHA-256 that generate unique, tamper-proof hashes. Any changes to the blockchain are easily detected by the network and rejected, preserving a perfect audit trail of all past records.

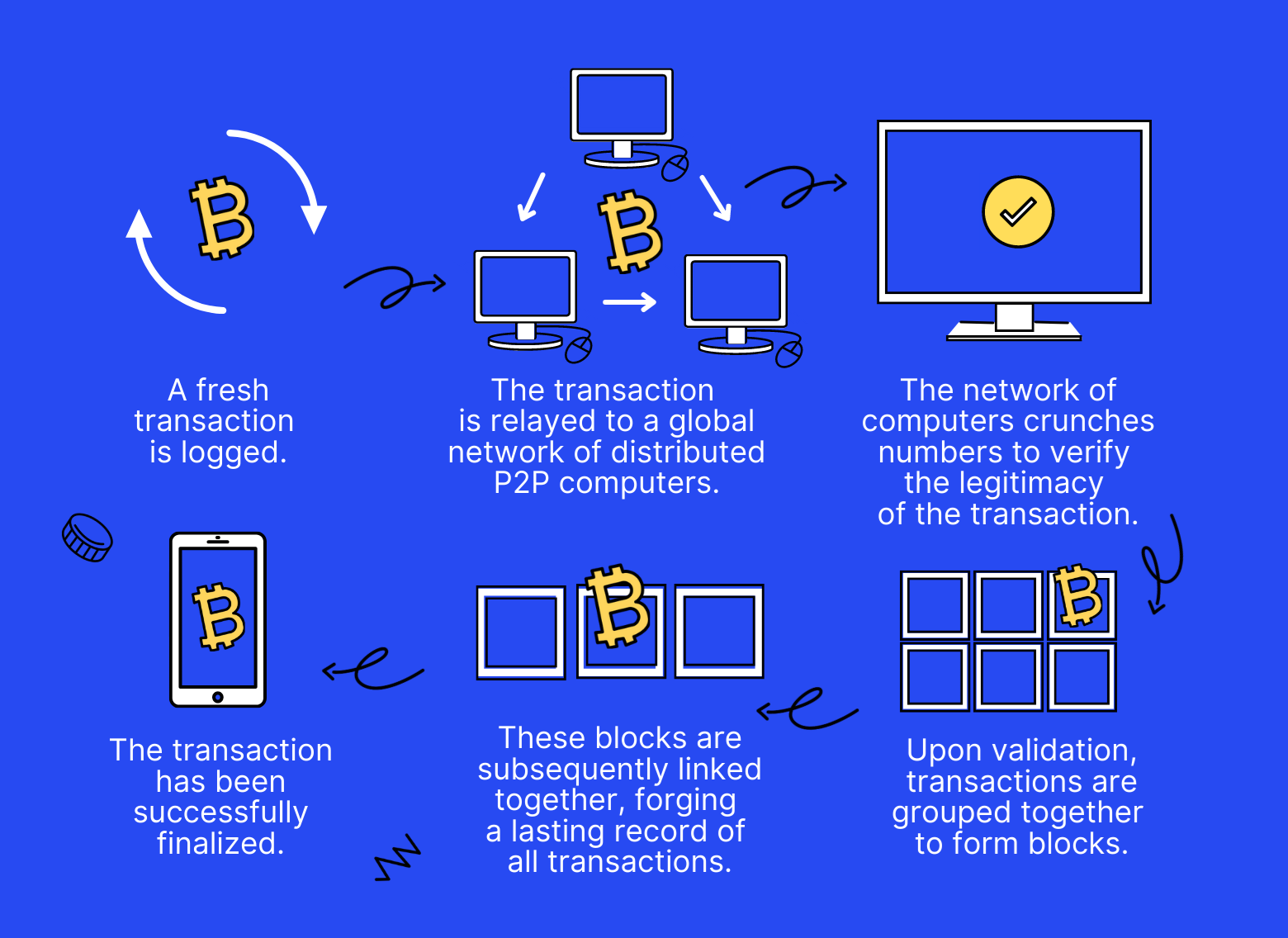

New data is added to the blockchain through a consensus mechanism, whereby a majority of nodes on the network verify and approve the legitimacy of transactions. When consensus is reached, a new block is created, appended to the chain, and distributed across all nodes (Pic. 2).

In public blockchains, nodes that successfully verify new transactions first are incentivized with a reward, typically in the form of the network's native cryptocurrency. This process is known as "mining". Miners use powerful computers to solve complex cryptographic puzzles and validate blocks of transactions, securing the network in a decentralized way.

In fact, there are two main ways of reaching consensus on a blockchain:

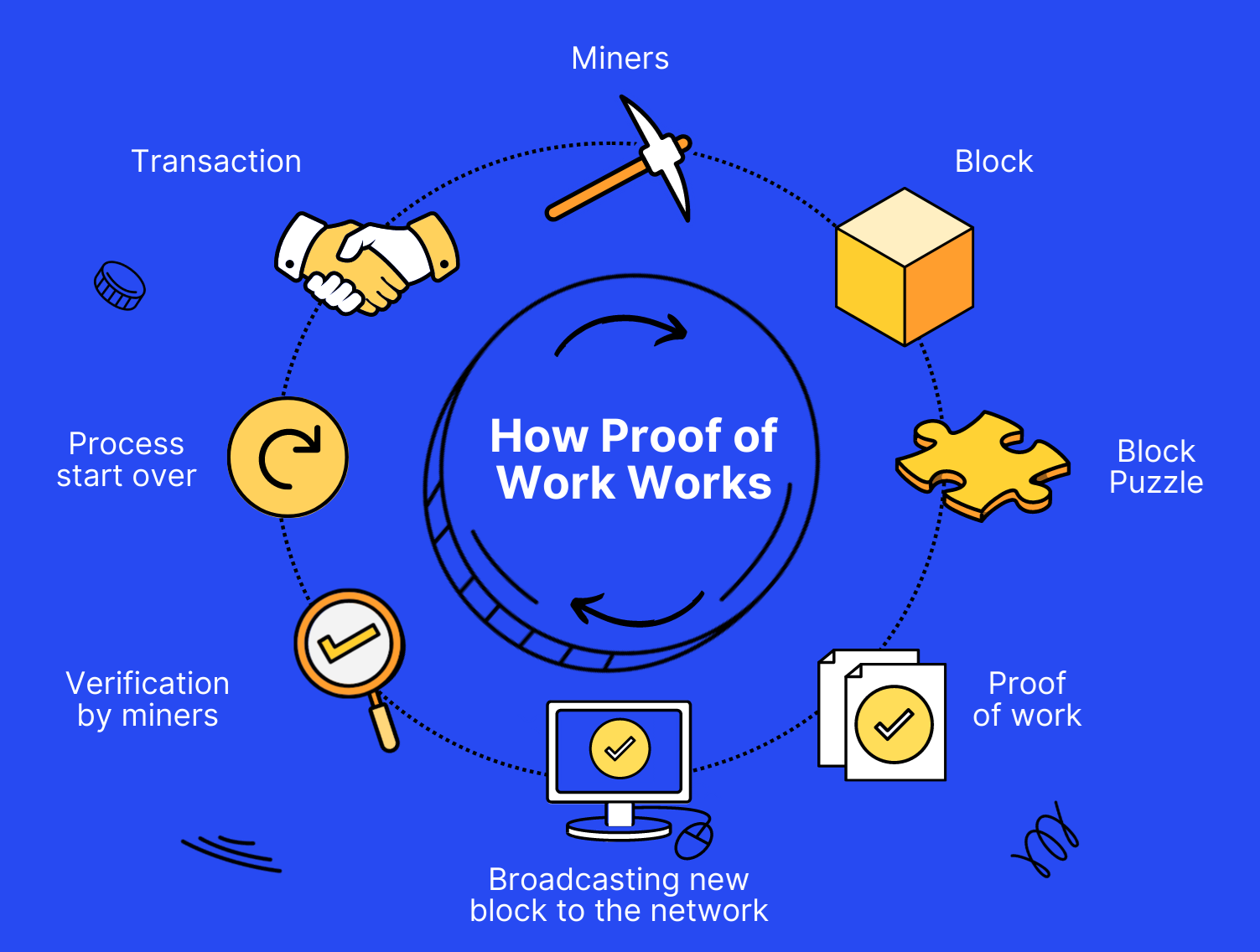

- Through proof-of-work (PoW): In PoW (Pic. 3), nodes compete to solve cryptographic puzzles and verify transactions. The first to solve the puzzle is rewarded with tokens.

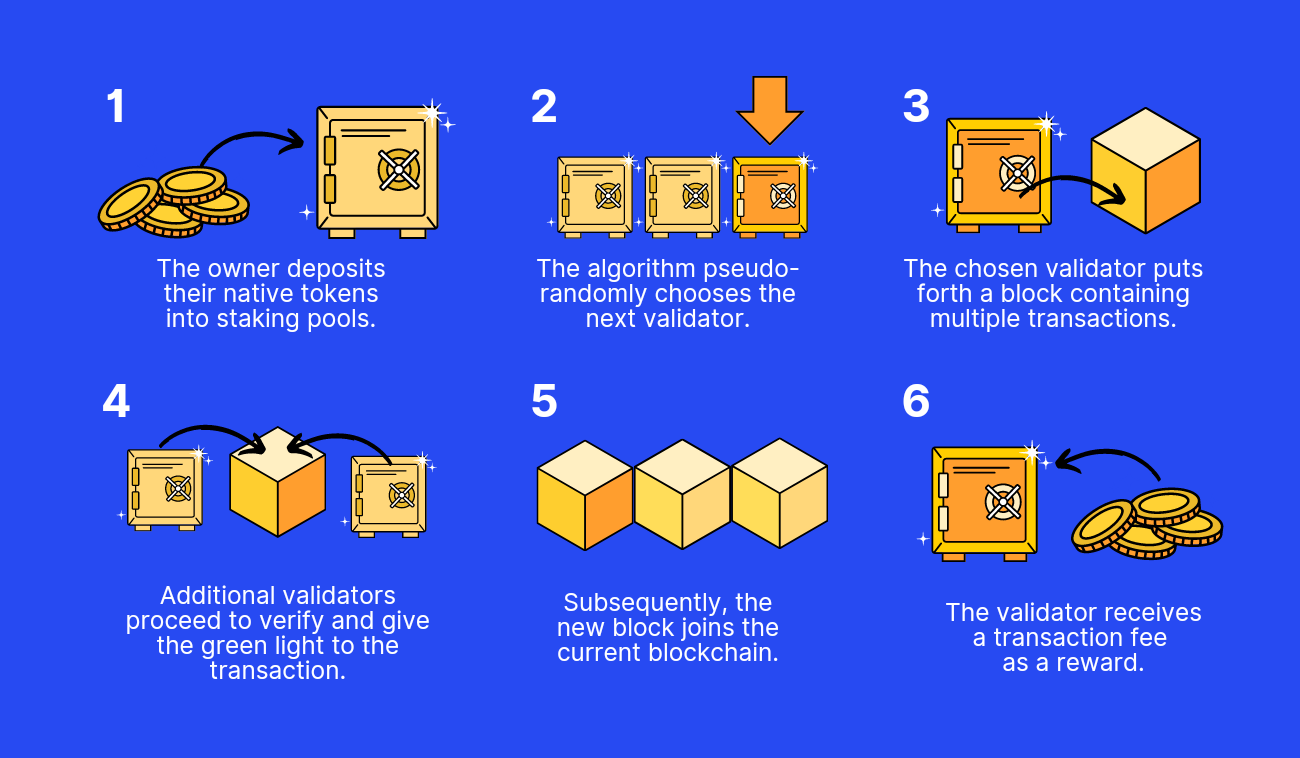

- Through proof-of-stake (PoS): In PoS (Pic. 4), nodes deposit their tokens into a pool for a chance to earn rewards by verifying transactions. The more tokens a node stakes and the longer they stake them, the higher their chance of being selected to validate transactions and earn rewards.

👉 Think of blockchain as a highly obsessive and transparent accounting system maintained by a network of strangers. This network establishes strict rules to guarantee that each member records the exact same records of events, like daily temperatures or coffee sales, in a shared digital ledger. Once data is recorded and approved by most of the network, it becomes nearly impossible to modify as more records get added. Outsiders can then review this transparent and tamper-proof ledger to see that, for example, it was 67 degrees in Austin at 3 pm on July 4th, or that 350 cups of coffee were sold by the downtown shop last Friday. And of course, the first unwritten rule of blockchain club is: you always talk about blockchain club. Members are incentivized through rewards to keep the network secure and running.

Blockchain vs. Database

Blockchain provides solutions to major flaws inherent in traditional databases:

- Databases are typically stored on centralized servers. This makes them vulnerable to attacks, downtime, and data loss. Blockchain uses a distributed network model, improving uptime and security.

- Centralized databases are expensive to maintain as the costs are borne by a single entity. Blockchain storage costs are distributed across its network, reducing costs exponentially.

- Centralized systems can be prone to censorship since they have a single point of control. Blockchains are decentralized, making them extremely censorship-resistant. No single person or organization can shut down the network or restrict access to data.

But What Is the Point of All This Blockchain Business?

Imagine a digital space where anyone can contribute information, no one can alter it, and it's not controlled by a single person or organization. That's what public blockchains offer. Rather than having one entity keeping tabs on everything, the responsibility is shared among everyone in the network.

While this concept may be shrouded in tech jargon like "distributed ledger," "peer-to-peer," and "cryptographically hashed," these phrases simply refer to the fundamental properties of blockchains.

In other words, blockchain allows internet strangers to reach consensus and share information freely without compromising privacy or giving up control to a central authority. How’s that for a bit of empowerment?

When and Why Blockchain Was Invented

Blockchain technology was invented in 2009 to power bitcoin, the first decentralized digital currency. By using a blockchain to track bitcoin transactions, Satoshi Nakamoto solved the double-spending problem and enabled peer-to-peer electronic cash for the first time.

But blockchain's potential extends far beyond cryptocurrency. Its ability to create transparent yet secure networks of trust resonated with people around the world, and developers began exploring other use cases.

Blockchain Technology in Cryptocurrency

Blockchain's most famous (and perhaps most contentious) application is cryptocurrencies. Digital currencies like bitcoin and ether let you buy goods and services just like you would with physical cash. However, unlike cash, cryptocurrencies rely on blockchain technology as a distributed ledger and a robust cryptographic security system, ensuring that online transactions are always recorded and protected.

👉 The terms bitcoin and blockchain are often used interchangeably, but they actually refer to two distinct things. Bitcoin, the first-ever blockchain application, emerged in 2009 as a crypto system utilizing distributed ledger technology. The Bitcoin blockchain refers to the underlying technology, while the bitcoin cryptocurrency denotes the currency itself.

Today, there are over 20,000 cryptocurrencies with a total market cap of around $1 trillion, with bitcoin dominating the market. So, what's behind the recent surge in popularity?

- Blockchain's security makes theft more difficult since each cryptocurrency has a unique, irrefutable identifier linked to a single owner.

- Cryptocurrencies reduce the need for individual currencies and central banks, allowing for global transactions without currency exchanges or central bank interference.

- Some early adopters have become incredibly wealthy due to cryptocurrency speculation. However, whether this is a net positive remains to be seen, as speculators may not prioritize long-term benefits.

- Major corporations have embraced blockchain-based digital currencies for payments. For instance, in February 2021, Tesla invested $1.5 billion in bitcoin and began accepting it as payment for its cars.

Of course, there are valid criticisms of blockchain-based digital currencies. The lack of regulation and market volatility due to speculation have caused some people to lose significant sums. Additionally, the long-term stability and adoption of cryptocurrencies are still uncertain.

👉Looking for a place to trade and multiply your crypto? Look no further than Bitsgap!

Bitsgap is your central hub to manage all your linked exchange accounts (in fact, 15+!) from a single interface. No more space-hopping to monitor holdings, scout new trades, or place orders. Bitsgap is your golden ticket to the expansive world of crypto.

Connect your exchange accounts to access a broader range of digital assets from a single screen, benefit from smart and automated trading tools, maintain complete control of your far-reaching crypto portfolio, and uncover the most rewarding trades across platforms!

Blockchain Use Cases: Blockchain Applications

Cryptocurrencies may steal the limelight, but blockchain experimentation spans across various sectors.

👉 For instance, Walmart has utilized blockchain to trace produce from farms to its stores, aiding in accountability during disease outbreaks.

Moreover, blockchain use cases are rapidly expanding as blockchain converges with other emerging technologies.

Some examples of blockchain applications include:

- Permanent and verifiable records. Blockchains can be used to create immutable records of both static data (e.g. land registry) and dynamic transactions (e.g. asset transfers). This allows for audit trails that can be traced indefinitely.

- Enhanced security and transparency. Blockchains make it possible to track the origin and status of any transaction. This helps prevent data breaches by ensuring companies know exactly where their information came from and where it went.

- Automated contract execution. Blockchains support "smart contracts" — programs that can automatically trigger transactions when certain conditions are met. For instance, a smart contract could release payment to a vendor once goods have been received and verified.

However, the long-term success and necessity of the blockchain systems remain uncertain, as many businesses jumped on the bandwagon without a clear understanding of their implications.

Blockchain Example

Company X leaps on the blockchain bandwagon, eager to jazz up its supply chain management and shave off some pesky costs. They join forces with a blockchain developer to cook up an ingenious solution.

The plan? Simple! Company X sets up a groovy process that gets every party in the supply chain — think factories, ports, vendors, and retail spots — to boogie along and scan product codes at each step of the way. The info from each scan gets etched into the blockchain, leaving an unchangeable record of the product's journey.

Thanks to the nifty data on the blockchain, Company X can now peek into its supply chain like never before, sniffing out bottlenecks and inefficiencies. The super-duper auditable records make accounting and compliance as easy as pie. Plus, customers can now sneak a peek at the origins of their goodies, confirming they're as fresh and genuine as they claim to be.

As a result, Company X ushers in an amazing new era for its supply chain that is entirely blockchain-based. With a crystal-clear view of their inventory and product flows, they're now primed to optimize operations, minimize waste, win the hearts of their customers, and outshine the competition. Sure, they had to jump through some hoops to get the blockchain show on the road, but the cost and efficiency rewards make it all worthwhile. Company X's smashing success is a testament to the transformative power of blockchain in supply chain management.

Benefits of Blockchain Technology

Here are the key benefits of blockchain technology:

- Enhanced security. Blockchain employs cryptography, decentralization, and consensus mechanisms to create a tamper-proof system. With no single point of failure and no ability for a single user to change records, blockchains are highly secure.

- Improved efficiency. Blockchain's transparency and smart contracts can streamline slow, manual business-to-business transactions, especially those involving third-party compliance checks. By automating these processes, blockchains can cut out inefficiencies and accelerate deals.

- Faster auditing. Blockchain records are chronologically ordered and immutable, meaning they cannot be changed over time. This makes the audit trail transparent and easy to follow, speeding up auditing processes. Auditors can quickly verify the integrity of records and trace transactions from start to finish.

- Cost reduction. Blockchains can decrease costs associated with transactions, record-keeping, and auditing. Their decentralized networks and automation reduce the need for intermediary third parties to facilitate deals, maintain ledgers, and ensure regulatory compliance.

- Increased transparency. The distributed, chronological ledgers provided by blockchains give all parties a transparent view of transactions, enabling higher levels of trust. This transparency also allows for easier tracing and verification of records over time.

Blockchain Issues and Challenges

However, blockchain is not without its challenges:

- Lack of adoption. Without widespread adoption, blockchains will struggle to be effective and scalable. However, according to APQC, only 29% of organizations are currently using blockchain.

- High costs. Blockchain implementation requires significant investments in software, engineering, and administration. The costs may be prohibitive for some organizations.

- Scalability issues. Public blockchains like Bitcoin and Ethereum can only process a few transactions per second, limiting their viability for large-scale applications. Blockchain must improve its speed to achieve widespread adoption.

- Security and privacy concerns. Blockchain applications often require smart transactions and contracts to be linked to real identities, raising privacy and data security concerns. Private or permissioned blockchains may mitigate some issues.

- Regulatory uncertainty. The lack of clear regulations creates risks around fraud, scams, and market manipulation. Some countries have banned cryptocurrencies like bitcoin, while others struggle to regulate blockchain networks effectively.

- Criminal activity. The anonymity and decentralization of some blockchains have enabled theft, fraud, and illicit activity. Stricter security protocols and regulations could help curb criminal use of blockchains.

- Energy consumption. The proof-of-work consensus mechanism used by some blockchains requires immense amounts of energy. This raises environmental concerns and centralizes mining power. Alternative consensus models could help.

- Vulnerability to 51% attacks. Decentralized blockchains that use proof-of-work are at risk of 51% attacks, where groups gain control of the blockchain by controlling 51% of the mining power. This threatens security and trust in some blockchain networks.

- Shortage of skilled workers. There is a lack of available talent to develop and implement blockchain solutions, leading companies to offer very high compensation. Training programs could help address the blockchain skills gap.

- Interoperability issues. Most blockchains cannot communicate or share data with other blockchains, limiting their functionality and adoption. Standards and integration solutions are still needed.

- Integration challenges. Integrating blockchain with legacy database systems can require rebuilding entire networks or developing complex integration strategies. This deters adoption, especially for organizations lacking blockchain expertise.

- Private key management issues. In decentralized networks, the loss or theft of private keys can lead to loss of data access or funds with no way to recover. More robust key management solutions are required to prevent irreversible loss of access.

👉 While numerous and complex, many of the challenges facing blockchain technology are typical growing pains associated with new technologies. Promoting the widespread adoption of blockchain will require both technological improvements to the core infrastructure as well as a persuasive business case to drive buy-in across industries.

Can Blockchain Be Hacked?

Yes, as was previously discussed, blockchains might find themselves in the crosshairs of 51% attacks. However, pulling off such a scheme is no walk in the park, especially when it comes to bigwigs like Bitcoin or Ethereum.

That said, it's not entirely out of the realm of possibility, and there have been instances where these attacks got the better of a blockchain project. When things go south, it's time for the project to roll up its sleeves, adapt, and reorganize to shield itself from any future hacking attempts.

Can Blockchain Exist without Mining?

At the moment, blockchains do seem to need a dash of mining magic. However, alternatives exist, such as the energy-saving proof-of-stake (PoS). PoS selects nodes to validate blockchain transactions based on the number of tokens they hold.

There’s also proof-of-history (PoH), the brainchild of the Solana Project, which is similar to proof-of-elapsed-time (PoET). PoH employs crypto-tricks to track time's passage in a verifiable way, letting the network hit consensus without breaking a computational sweat.

Can Blockchain Replace Central Banks?

Chances are slim that blockchain will give central banks the old heave-ho. To be frank, it's more plausible that central banks would cozy up to blockchain and make it their own. This love affair could lead to a swifter, more budget-friendly management system. What seems more likely in the grand scheme of things is that banks, crypto, and blockchain will keep strutting their stuff right next to each other, sometimes merging paths and other times diverging in separate directions.

Bottom Line: Will Blockchain Change the World?

While the future of blockchain is bright, we have a long road ahead. There are still challenges to overcome before widespread adoption, as companies work to adjust services and reap the rewards. But the possibilities are endless.

Blockchain will change life as we know it. The mundane will be made more efficient. The complex will be made simple. Gatekeepers will be removed, and opportunities will abound.

While there is little doubt that blockchain will play a critical role in both the public and private sectors, the reality of this future may still be farther away than many anticipate. To bridge the gap, the focus must shift to making this revolutionary technology accessible and user-friendly for all.

FAQs

How Does Blockchain Work?

Blockchain is a decentralized digital ledger that securely stores transaction data across a network of computers. Each transaction is verified, encrypted, and added to a "block," which is then linked to the previous block, forming a chronological "chain." This structure ensures the integrity and immutability of the stored data, as altering any information in a block would require consensus from the majority of the network.

What Is Blockchain Explorer?

A blockchain explorer is a search engine or browser-like tool that allows you to access and navigate the details of a blockchain network. It provides insights into transaction history, balances of addresses, and the status of individual blocks. Blockchain explorers are essential for verifying and monitoring activities on a blockchain, offering transparency and enhancing trust in the decentralized system.

What Blockchain Is Good for and Where Can It Be Used?

Blockchain technology excels in scenarios where trustless management is crucial, fostering a more democratic and cost-effective system.

Leveraging distributed resources, blockchain-based projects can operate with minimal expenses, as costs are evenly distributed among participants. Moreover, these services are incredibly resilient, making it challenging to shut down or restrict access without significant effort.

Beyond digital currencies, blockchain offers a wide array of practical applications, including supply chain management, content hosting, data storage, identity protection, remittance, and more, showcasing its versatile potential in various industries.

What Are Blockchain Technologies?

At its essence, blockchain technology is a versatile system designed to record and manage various types of data, be it financial or otherwise. The simplicity of the underlying blockchain concept belies its true potential, as the unique and innovative applications developed by projects or businesses harnessing this technology are what truly set it apart.

Are Blockchain and Bitcoin the Same?

Many people believe that the blockchain and Bitcoin are one and the same, but they are not. While Bitcoin does use the blockchain, they are different. Blockchain applications are far wider than just digital currencies.